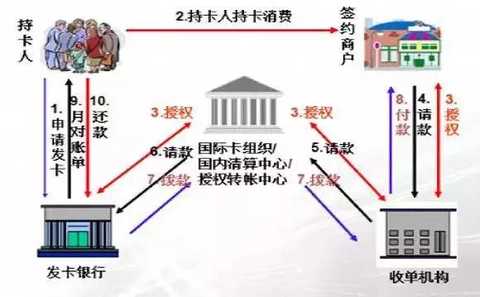

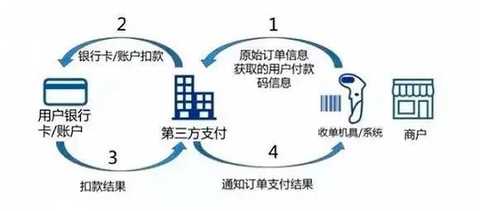

The fund manager's mouse warehouse, said that the capital preservation has become a huge loss, and the fund is pitted to the [fund exposure station]! The credit card was stolen without any reason, the bank deposit became insurance, and the financial management was cheated, please poke [Financial Exposure Desk]! Can UnionPay’s “Second Entrepreneurship†and market transformation really stimulate China’s mobile payment landscape? Wen|Miao Yiwei Source|Interface (ID:wowjiemian) In the summer of 2017, Apple, which has always been known for its “high cold†in marketing, joined hands with UnionPay in China to start a near-end payment marketing in China that enjoys a 50% discount on the use of “Apple Pay+ UnionPay†for one week. Just one month ago, China UnionPay also joined nearly 100,000 merchants to push the QR code to pay, and launched the "62 UnionPay cloud flash to pay the people Sheng Hui." UnionPay announced its participation in the mobile payment war with two rounds of marketing subsidies of several hundred million yuan and two major payment methods of “UnionPay Cloud Flash Paymentâ€. However, at this time, the actual application of the China Mobile payment QR code has been more than three years, and it has been nearly one year since the central bank officially recognized the payment status of the QR code. The market is full of doubts about UnionPay. Is the Big Mac in the era of card-based payment in the fierce Internet mobile payment wars “have been late†and thus “missed the opportunityâ€? Difficult breakout "Compared with the innovation of China's third-party payment institutions, the UnionPay side has added safety to its choices in terms of payment security and efficiency, and put efficiency in a secondary position." A payment industry Senior people told the interface journalist: "At the policy level, the innovative application of UnionPay has been strictly controlled by the regulatory authorities. In contrast, the third-party payment institution is undoubtedly a disruptive innovation to China's original payment system and enjoyed for several years. Regulatory gaps and policy dividends." Looking at the moment, the competitive pressure faced by UnionPay is not small. In terms of payment methods, China's QR code payment has already occupied the mainstream of offline high-frequency micropayments. UnionPay's main NFC payment is used. In terms of competitors, Alipay and Tencent (Tianfutong, mainly including WeChat payment) And QQ wallet) in the domestic third-party mobile payment market share of 53.7% and 39.51%, respectively, occupying 93% of the market, while UnionPay's market share is less than 1% (Easy Think Tank first quarter data this year). Under the stable situation of the duopoly, China UnionPay, in conjunction with more than 40 commercial banks and third-party payment institutions such as Jingdong Payment, launched a "62" mid-year promotion with a large discount, and entered the battle. Taking UnionPay's 62-year promotion as an example, the data disclosed by UnionPay showed that during the “62†event, the number of new users of UnionPay QR code increased by 402%. From the number of transactions, it took three-quarters of the number of transactions in the UnionPay QR code, including NFC payments such as Apple Pay and Huawei Pay, and the average daily transaction volume was “62â€. Activities increased by 308%. It is worth noting that UnionPay did not disclose the absolute base of the relevant ratio. People from UnionPay told the interface news that although the growth rate of UnionPay is quite high, in terms of the absolute value of market share, it is still far from being able to compete with the two giants. However, the two self-defense counterattacks that the UnionPay started are not to be underestimated. Perhaps it is just the beginning of the curtain. Behind it is the ambition of the second-time entrepreneur who has painstakingly paid for the big brother in the payment industry. Second venture On March 31 this year, UnionPay President Shi Wenchao released its 2017 business objectives. UnionPay said that due to the slow growth of electronic payment business, UnionPay's profit growth target was reduced from 43% to 20% in 2017, leaving room for its own reform. "In short, the competition at this stage is the competition of market share. All strategies must be carried out around the share. We must "make up our minds, not afraid of sacrifice, eliminate all difficulties, and strive for victory!" "Wen Wen also made a military order in the internal publication of the 15th anniversary of the establishment of UnionPay in March this year, which is in line with the joint strong breakthrough action three months later. However, a member of the UnionPay said to the interface news that so far, UnionPay has not set a clear and specific market share target. Over a decade of franchise rights have disappeared, and the competition in the mobile market has become fierce and questioning, which has enabled UnionPay to begin a top-down reflection and reform under pressure from both inside and outside. “Why is the financial strength, system strength, and risk control ability the best financial institutions, but can't take the lead in the mobile Internet era?†Wen Zhaochao sent a question to all UnionPay people in the internal issue. "The reason is in the last hundred meters." Shi Wenchao wrote in the email: "When our perspective is from card issuance and receipt to real terminals, ie cardholders and merchants, we can find a large and highly discrete audience, which is making our customers face the terminal. The demand is complex and changeable, the coordination costs between institutions are high, the resources are scattered and the strength is weak. The focus of attention and assessment of various institutions is different. It is difficult to make a hole and a hole. The entire cooperation chain can not find the pain points of the users. The hand of the hand, which brings the risk of the user being abandoned or bypassed." As a result, UnionPay has fully entered the “secondary ventureâ€. "Is the future payment carrier large enough to be issued by a single UnionPay card to a regulatory body that is issued by the rule, with a brand identity and a payment carrier that can be used in the network?" Wen Zhao proposed that UnionPay will pursue the next payment method. "To the position of "paying the brand". He positioned the market competition of the new stage of UnionPay as “the catch-up†and proposed that in the future, UnionPay will aim at the overall network and carry out resource-wide allocation of the whole product. The unified brand “UnionPay Cloud Flash Paymentâ€, which is specially designed for the mobile Internet, is undoubtedly one of the achievements of this concept. In recent years, UnionPay has continuously added improvements to the “Cloud Flash Pay†brand. At present, "UnionPay Cloud Flash Payment" has included three payment methods based on the "quartet mode" - smartphone PAY (a type of NFC near-field payment), wearable device payment and two-dimensional code payment. Quartet VS Tripartite It is worth noting that the payment products launched by UnionPay are similar to Alipay and WeChat on the terminal (Alipay launched NFC near-field sound wave payment around 2014), but there are fundamental differences in business models. The core of the traditional payment method is the “quartet modeâ€. The participants include card organizations (such as UnionPay), card issuers (generally commercial banks), merchants and acquirers. In the Quartet mode, SamsungPay and ApplePay “load†the bank card into the mobile phone. When the mobile phone is swiped, it is still a bank card. The clearing method behind it is the same as the physical card. Payment industry "quadruple mode" In the “quartet modeâ€, funds are transferred directly from the issuing bank to the acquiring bank, without the card organization, and the flow of funds and the flow of payment information are separated. As a card organization, UnionPay specializes in clearing functions and related standards development and market order maintenance. Commercial banks are responsible for issuing cards and payments. The acquiring institutions are responsible for the development and management of special merchants, authorization requests, bill settlement and other activities. The benefits mainly come from the division of service fees and service fees for special merchants. The "three-way model" is a subversion of the original "quartet mode", which was called "over-the-top pass". In the “three-way modelâ€, third-party payment companies such as Alipay and WeChat Pay have become “wallets†through virtual accounts. The user refills the virtual account through the bank account, and then through the virtual account transaction, the bank loses the transaction information and becomes the capital channel, while the third-party payment institution undertakes the payment and the “not supposed to have†clearing function, and the regulatory agency also Concerned about the risk of depositing funds in the tripartite model. Payment industry "three-way model" Proponents of both models have been standing in line in recent years. The “Quadruple Model†side, together with UnionPay, includes some commercial banks, Jingdong (Jingdong Flash Payment), VISA and other traditional payment institutions, as well as emerging Apple Pay. On the other hand, Alipay and WeChat payment became the most successful representatives of the “three-party modelâ€. According to the industry, the reason why the "three-party model" can quickly occupy the market in a short period of time is that its industrial chain is short, and the role of not involving UnionPay, mobile phones and banks has also been instrumentalized. Users, merchants and payment companies can complete the cooperation. The entire transaction, the ecosystem is simple. The Quartet model requires multi-party – UnionPay, banks, users, merchants, and even mobile phone manufacturers, and the ecosystem is complex. But the two modes are not irreconcilable. In July of this year, the “Jingdong Flash Payment†product jointly launched by UnionPay and JD.com was in the forefront of exploring the integration of two payment modes. On July 19th, Jingdong Finance announced that it will jointly launch a new NFC payment payment with Beijing UnionPay – Jingdong Flash Pay. In addition to online consumption in Jingdong Mall, users can use the “Cloud Flash Pay†POS machine of UnionPay’s nearly 10 million lines. Using Jingdong Flash Pay, UnionPay has turned the accounts of JD.com and Meituan into an aggregate payment account based on bank card accounts. Unlike the “three-way modelâ€, this time, UnionPay and JD.com changed the “Staged Wallet†(traffic wallet) used by the third-party model to cut off capital flow and information flow into “Passthrough Wallet†(invasive wallet), innovation Launched "Electronic Account Cloud Flash Payment". The person in charge of UnionPay Beijing Branch said that in the electronic account cloud flash payment mode, the payment institution and its account are only “channelsâ€, which are positioned as channels for obtaining and diverting banks, and accessing the UnionPay network to achieve controllable and credible Visible, available channels. On the one hand, this model does not cut off the information exchange between banks and card organizations to merchants and cardholders like other “retained wallet†applications. Funds are still “from banks and banksâ€, and the basic position of banks has not been weakened. Secondly, it not only realized the bank's indirect marriage with the Internet organization to achieve online mass-acquisition, but also made the card-free fast payment channel of e-banking stronger and stronger, and also provided the integration of "three-party mode" and "quartet mode". Feasible solution. Through cooperation with Internet organizations such as Jingdong, which has strong customer operation capabilities and flexible marketing incentives, UnionPay is trying to change the problems of low payment, inactive customers and insufficient scenario building capabilities. With JD.com's heavyweight player's recognition of UnionPay's "Quadruple Model" and NFC payment and UnionPay QR code, Jingdong E-commerce and other scenarios are becoming a new application scenario for CUP expansion and an important source of increased activity. The joining of Jingdong is just the beginning. With the continuous opening of the ecological model of UnionPay, more and more partners joining the “Platform†of UnionPay payment will become another source of competitiveness of UnionPay payment products. Shi Wenchao once said that “it is also a trend to set up a payment-centered “diversity alliance†to become a development option that many institutions may choose.†QR code VS NFC Not only does the business model have a "four-party" and "three-party" model dispute, from the NFC payment to the first opportunity, to the two-dimensional code payment later, the industry has also had major differences in payment terminals. UnionPay is the biggest fan of NFC payments. NFC (Near Field Communication) payment, full name of short-range wireless communication technology, compared to the two-dimensional code, it was born earlier, is the payment method that UnionPay has strongly promoted. In UnionPay's view, compared with other payment terminal methods, NFC's acceptance network does not need to pay online, which can avoid the embarrassment that cannot be paid because the mobile phone has no signal. In addition, NFC mode further eliminates the need to unlock the phone, open the app, and click scan code. More complicated is that the NFC's UnionPay payment token (Token) replaces the bank card number for transaction verification technology, which can reduce the possibility of leakage of the card number in information storage, transmission and other aspects, and is also more secure. However, NFC technology is still not fully mature, and the high failure rate of payment, the difficulty and cost of user training, and some users who are temporarily fresh are gradually giving up. And after experiencing a wave of twists and turns, UnionPay also missed the best time window for China's NFC development. Even ApplePay and SamsungPay, which were later launched with Apple and Samsung, lost time. At present, the effect is not satisfactory. The two-dimensional code payment technology born in UnionPay Lab, with the rise of smart phones, has become the most mainstream payment method in China in the three years after the two giants, Alipay and WeChat, have cultivated their habits. In 2017, in the entanglement of market competition, UnionPay passively joined the "two-dimensional code" battle. Although it is late, UnionPay Chairman Ge Huayong said that compared with other QR codes on the market, “the UnionPay QR code is in line with global standards; the second is higher security; the third is more complete services.†According to Ge Huayong, “In terms of transaction initiation, the first batch of commercial banks supporting cloud flash payment QR codes has exceeded 40. Internet companies represented by Jingdong, Meituan and Volkswagen Group have also opened to UnionPay QR code. In terms of transaction acceptance, more than 60 organizations have already supported the UnionPay standard QR code, and approximately 2.66 million merchant technologies have opened the UnionPay standard QR code service." However, "Because UnionPay's allies - 40 commercial banks, the app technology level of the various banks is uneven, the use of QR code to the user is not a problem." A UnionPay middle-level interface to the journalists said. "In short, although the current near-field payment market is still not accepted by most people, UnionPay is quite confident about the Quartet model and the prospects of NFC near-field payment. In the future, UnionPay will continue to adhere to the Quartet model and NFC payments. The terminal payment method, the two-dimensional code payment is mainly to supplement the payment method in accordance with the current market situation," said the person said. In addition, the online network that was launched on March 31 this year also has a certain impact on UnionPay. The two sides have a dual relationship of competition and cooperation. In the future, the payment clearing option chooses UnionPay or Network Link. Who can provide more favorable rates and who is more convenient? Both have become important conditions for institutional access to clearing. Is the Quartet mode or the Tripartite mode? Is QR code payment or near-field payment? Choose UnionPay or Network Link? Pay attention to payment security or payment efficiency? These challenges in front of UnionPay, the "big brother" in the payment industry, are not an alternative question, but a smart dance that requires courage, innovation and even balance. Can UnionPay’s “Second Entrepreneurship†and market transformation really stimulate China’s mobile payment landscape? Time will give the answer. Enter [Sina Finance and Economics Unit] Discussion Cotton Beach Towel,Cotton Beach Towels,Terry Cloth Beach Towel,Muslin Beach Towel Hengshui Dahan Textiles Co.,Ltd. , https://www.dh-towel.com

June 08, 2023